Key takeaways

• Pick the provider before the feature set, not after. Switching a digital payment solution after launch usually costs 4–8 engineering weeks; picking right on day one saves a quarter of runway.

• Three signals decide the choice. Country of incorporation, monetization model (one-time, subscription, marketplace), and tax-compliance appetite collapse the decision to two or three real candidates.

• Stripe is the safe default; Paddle wins when tax is the bottleneck. Stripe handles 195+ countries at 2.9% + $0.30; Paddle charges 5% + $0.50 but absorbs global VAT, sales tax and chargeback liability.

• Three monetization patterns cover 90% of products. One-time charges, subscriptions and marketplace splits — each maps to a different webhook flow, idempotency model and failure mode.

• Most revenue leaks come from five pitfalls, not from fees. Webhook drift, idempotency gaps, FX losses, broken 3DS and missed VAT registrations cost more than 0.4% of fee delta between providers.

Why Fora Soft wrote this digital payments playbook

Fora Soft has shipped revenue-bearing software since 2005 — more than 20 years — across video streaming, e-learning, telemedicine, marketplaces and SaaS booking. Most of those products live or die by the payment layer: an OTT service that loses 6% of charges to involuntary churn loses a full month of EBITDA every year; a marketplace that pays sellers two days late loses its supply side to a competitor that pays in 24 hours.

We have integrated Stripe Connect for marketplaces (Franchise Record Pool), wired pay-per-view + subscription on a video marketplace (Vodeo), built recurring billing and class booking on a fitness SaaS (AppyBee), shipped HIPAA-aware billing on a telemedicine product (CirrusMed) and stitched in-app purchases plus subscription tiers across e-learning at scale (BrainCert, Scholarly).

This guide is the answer we give founders, product leads and CTOs who land on a kickoff call asking the same three questions: which provider, which monetization model, and how do we keep the payments stack out of our way as we scale. We write to be useful first — if we save you a wrong choice and four weeks of rebuild work, that is the win we want.

Stuck choosing between Stripe, Paddle and Adyen?

Bring your country of incorporation, monetization plan and target volume to a 30-minute call — we will name the right provider on the call, free of charge.

The 2026 digital payments market in 90 seconds

Digital payments are the default now, not a feature. Statista puts total digital-payment transaction value near US$37.45 trillion worldwide in 2026, rising to a projected US$46.25 trillion by 2031 (a ~4.3% CAGR, 2026 forecast). The number that matters to a founder isn’t the trillions — it’s that your buyers already expect one-tap cards, wallets and local methods, and every point of checkout friction is revenue you earned and then dropped.

Three concrete shifts you should bake into the architecture you choose this year:

- Wallets are the new cards. Apple Pay holds about 57% of the US digital wallet share with ~87.5M US users in 2026; tap-to-pay volume is on track to grow ~150% by 2028. Treat wallet support as a launch requirement, not a v2 feature.

- ACH is eating B2B card volume. US B2B ACH volume rose 9.9% year over year to 8.1B transactions in 2025; the ACH network as a whole moved US$93T. If your buyer is a business writing $5K+ invoices, offering ACH/SEPA next to cards usually pays for the integration in two months.

- SCA enforcement is hardening. PSD2 strong customer authentication is fully enforced across the EEA, and PSD3/PSR will tighten SCA and exemptions — the texts landed in April 2026, but the rules apply ~21 months after publication, so the earliest real deadline is H2 2027. A weak 3D Secure flow now costs 5–10% of EU checkout conversion.

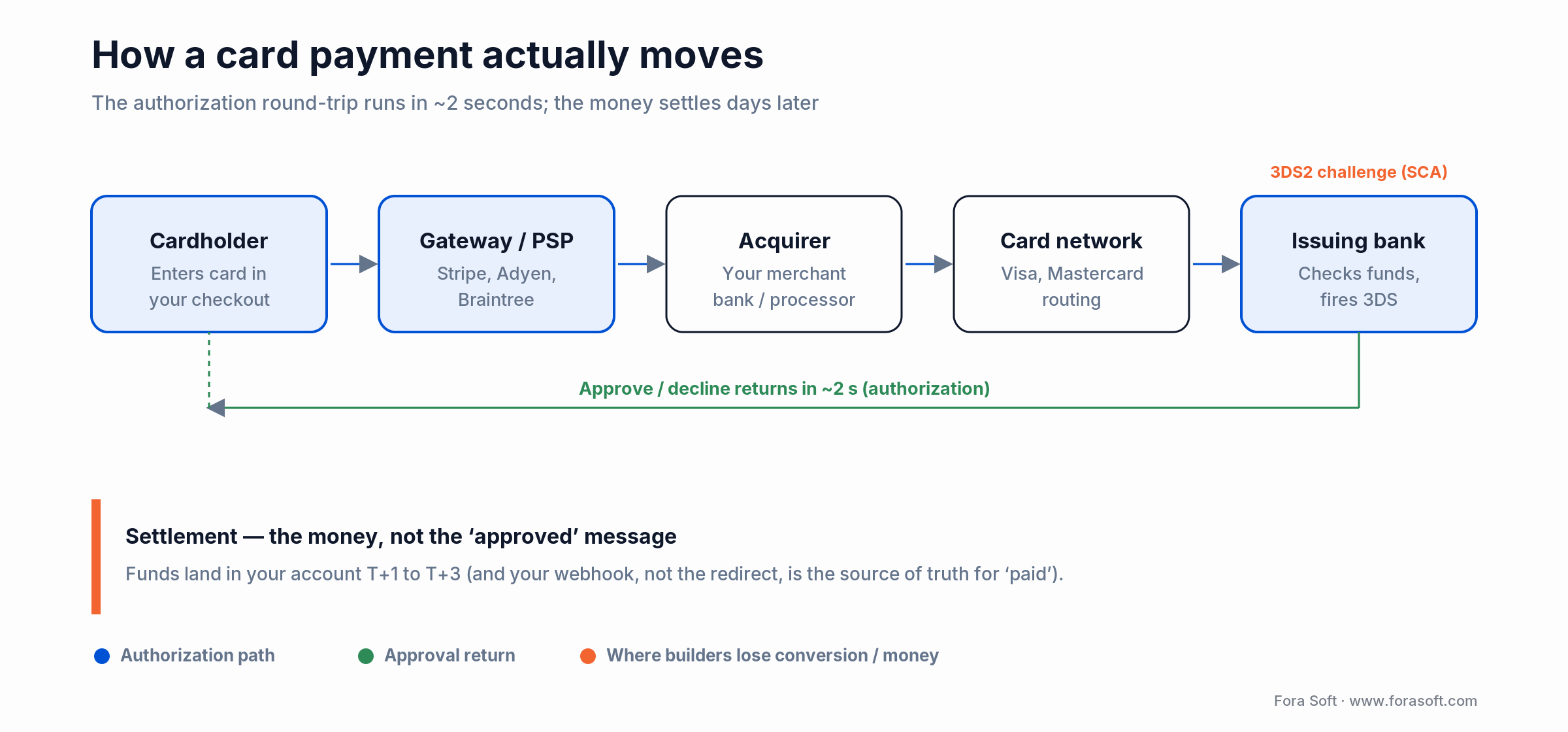

How a digital payment actually moves: the 60-second mental model

A clean mental model saves you a week of debate later. A modern card payment in your product crosses six systems in under three seconds:

Figure 1. The authorization round-trip is instant; settlement and webhooks are where ‘paid’ is really decided.

1. Your client. A user enters card data into a form — ideally hosted by the payment service provider (PSP) so card data never touches your servers.

2. The PSP gateway. Stripe, Adyen, Braintree, etc. tokenize the card, run fraud scoring, and forward an authorization request.

3. The card network. Visa, Mastercard, UnionPay or American Express route the authorization to the issuing bank.

4. The issuing bank. It checks balance and risk, may fire 3D Secure, and approves or declines.

5. The acquiring bank. Holds funds for settlement; pays out to your business bank on a 1–3 day cycle minus interchange and processor fees.

6. Your backend. Receives a webhook, updates entitlements, sends a receipt, posts to your accounting system.

Every architectural decision in this article comes back to those six steps: where card data lives, who carries PCI scope, where you handle 3DS, and how reliably step six lands in your database.

Reach for hosted checkout when: you do not have an in-house security team to maintain SAQ D scope — which is true for 99% of SaaS, marketplace and OTT teams under US$50M ARR.

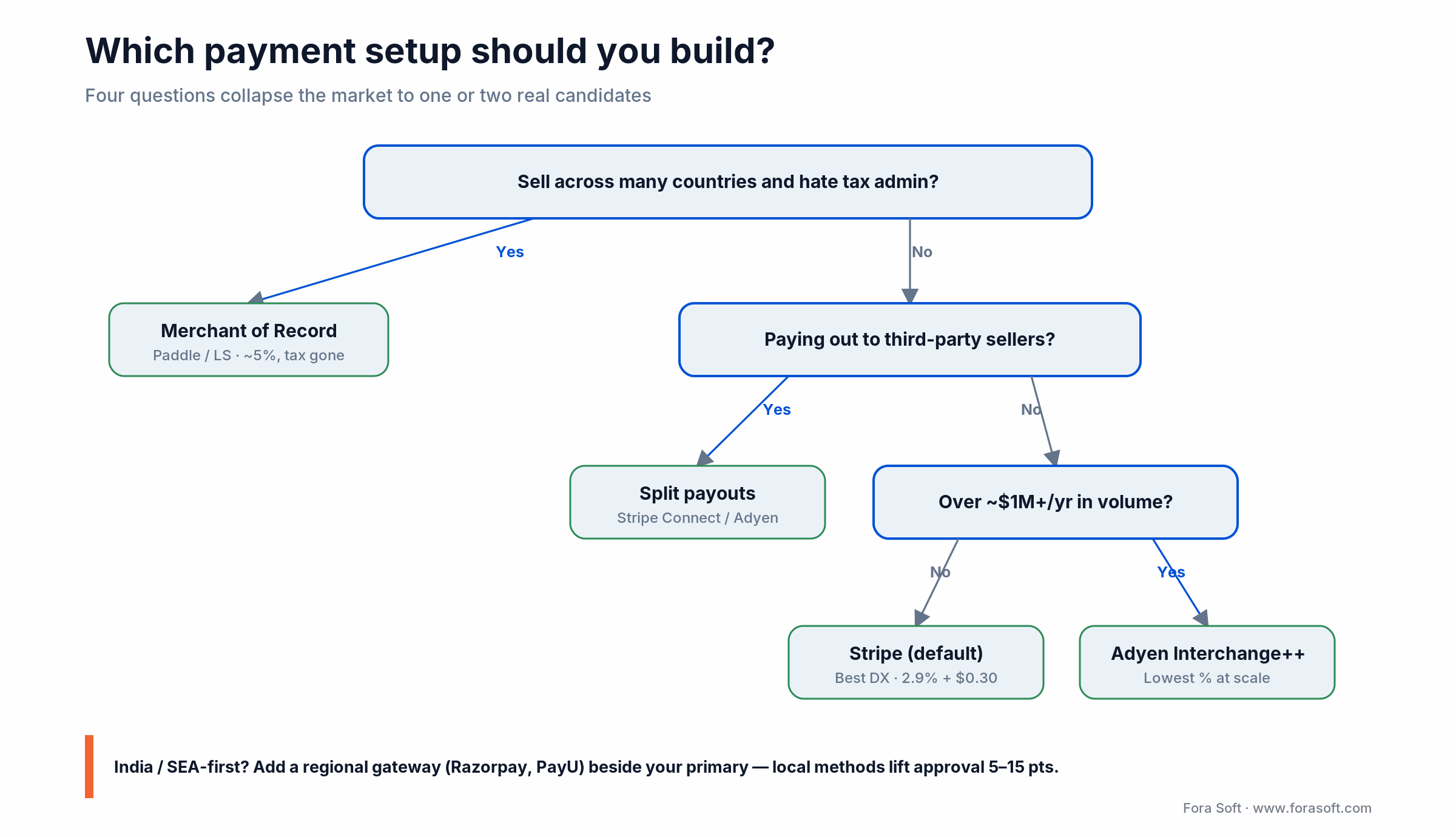

How to choose a payment service provider in five questions

Choosing a payment gateway — the payment service provider that actually moves the money — is close to a one-way door for your first year, so skip the provider blog comparisons until you can answer these five. They reduce the candidate list from twelve to two before you read a single fee table.

Figure 2. Four questions collapse the provider market to one or two real candidates.

Q1. Where is your business legally registered? Stripe will not onboard a Cayman entity; MangoPay only accepts EEA-registered businesses; Razorpay only accepts Indian entities; Adyen requires structured KYC most early-stage US/EU founders do not have. The country of registration — not the country of your customers — is the first filter.

Q2. What is your monetization model? One-time, subscription, marketplace splits, usage-based, in-app purchase — each implies a different webhook surface and different add-on cost. A marketplace on a flat-rate processor will overpay; a B2B SaaS on a Merchant of Record will overpay even more.

Q3. Where do your buyers actually live? If 70% of revenue will come from one country, optimize for that country's preferred methods (iDEAL in NL, Boleto in BR, UPI in IN, ACH in US, SEPA in EU). If buyers are spread across 20+ countries, you need a provider with native local methods, not just card support.

Q4. What is your tax-compliance appetite? If you are willing to register for VAT/GST in 30+ countries and run automated tax filings, a payment processor (Stripe, Adyen) is fine. If you would rather pay 1.5–2.5% extra to delete that work entirely, a Merchant of Record (Paddle, Lemon Squeezy) is the right move.

Q5. What monthly volume will you cross in 12 months? Below US$100K/mo, flat-rate Stripe wins. From US$100K–$1M/mo, you should be negotiating interchange-plus with Adyen or Worldpay. Above US$1M/mo, you can save 30–60 bps with a multi-provider routing layer.

Reach for a Merchant of Record when: you sell digital goods or SaaS to consumers in 20+ countries and you do not have a finance team that wants to register for VAT in each one.

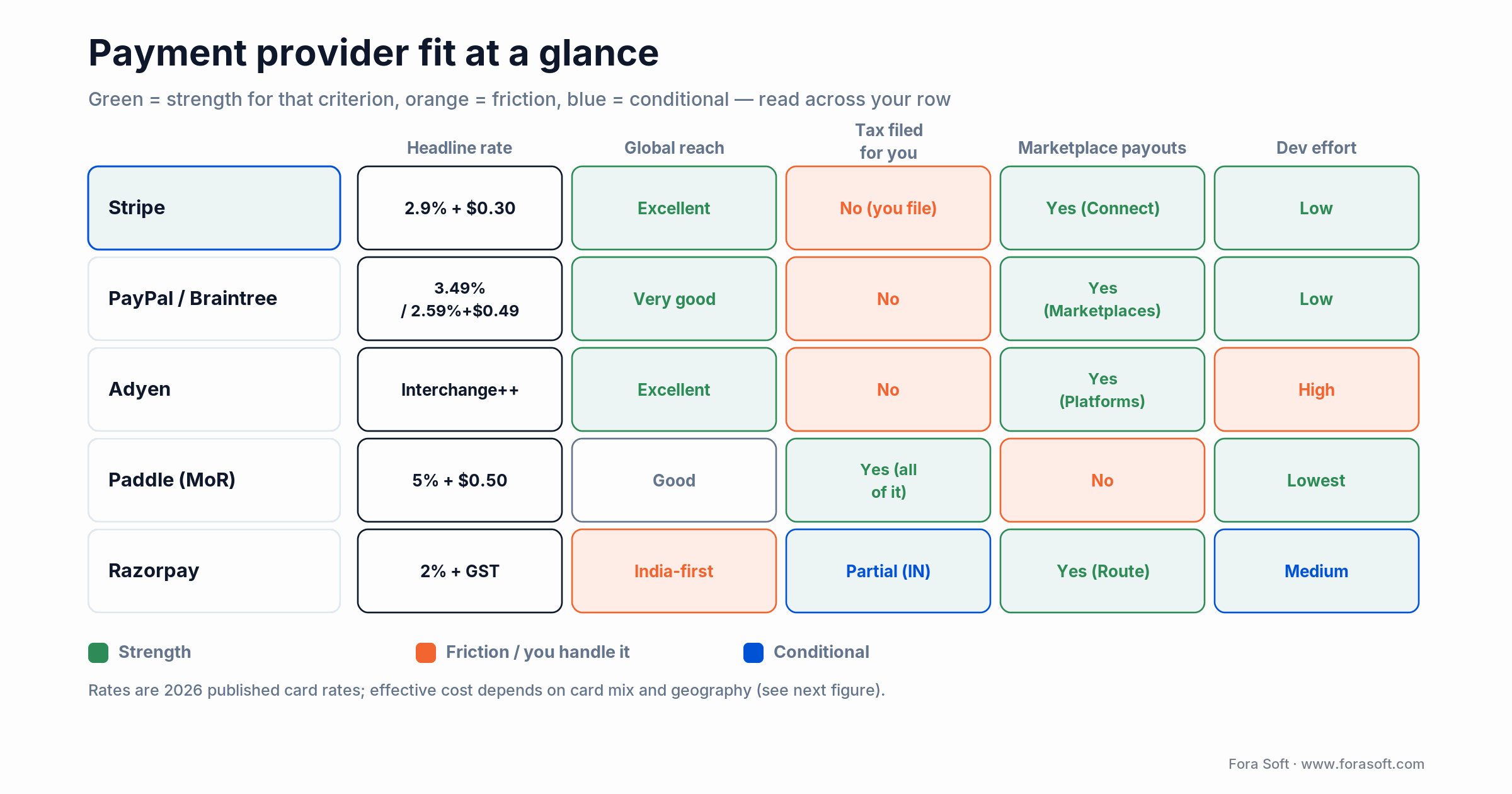

Stripe vs PayPal vs Adyen vs Paddle vs Razorpay: the comparison matrix

A side-by-side at the level of detail that actually moves a decision. Fees shown are public list prices for typical card-not-present transactions; large merchants negotiate down.

Figure 3. Read across your row: green is a strength, orange is friction you absorb, blue is conditional.

| Provider | Card fee | Coverage | Best for | Tax / MoR | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 US; +1.5% intl | 195+ countries | Default for SaaS, marketplaces, custom flows | You handle (Stripe Tax helps) | $15 dispute fee; flat rate at scale |

| PayPal / Braintree | 2.59–2.9% + $0.30–$0.49 | 200+ markets | Reach + buyer trust on consumer goods | You handle | Limited checkout customization on PayPal |

| Adyen | Interchange++ + ~0.25–0.50% + $0.12 | Global, deep EU/APAC | Enterprise, multi-region, $1M+/mo | You handle (enterprise-grade tooling) | Volume minimums; setup heavier |

| MangoPay | ~0.5% + fixed (varies) | EEA-strong, expanding | EU marketplaces, e-wallet flows | You handle | Heavy KYC; no Apple/Google Pay native |

| Razorpay | 2% domestic INR; 3% intl + GST | India only (incorporation) | India-first SaaS, UPI-heavy | You handle | No Apple Pay; geographic lock-in |

| Paddle (MoR) | 5% + $0.50 all-in | 245+ territories | B2C SaaS, digital goods, global indie | Paddle is the merchant; tax handled | Less control over checkout UX |

Stripe: the developer-first default

Stripe is what we recommend by default to roughly 70% of new clients, because the API surface is the cleanest, the published pricing and documentation are the most accurate, and almost every third-party (Chargebee, Recurly, RevenueCat, Avalara, Slack notifications, you name it) treats Stripe as a first-class citizen.

Why pick it

Five-minute Checkout integration, full programmatic control via Elements when you outgrow Checkout, native subscriptions, native marketplace splits via Stripe Connect, native tax registration in 50+ jurisdictions via Stripe Tax, and built-in fraud scoring with Radar. Local payment methods include iDEAL, Bancontact, SEPA, ACH, BLIK, OXXO, Klarna, Affirm and Apple/Google/Microsoft Pay out of the box.

Where it pinches

Flat-rate pricing means a US$5M/year merchant pays roughly the same percentage as a US$50K/year merchant unless they specifically negotiate. Dispute fees of $15 hurt low-ASP businesses. Stripe is also strict about high-risk verticals (CBD, adult, gambling, certain crypto flows) — if you are in one of those, plan for a backup processor.

Reach for Stripe when: you are a B2B SaaS, marketplace or subscription product registered in the US/EU/UK/CA/AU, doing under US$1M/mo, and your team values developer ergonomics over fee negotiation.

PayPal and Braintree: the broad-coverage incumbent

PayPal still moves a substantial share of consumer dollars; Braintree is its developer-friendly sibling acquired in 2013. Together they make sense when buyer trust matters more than checkout perfection — cross-border consumer goods, secondhand marketplaces, donations, B2C creator commerce.

Why pick it

PayPal as a payment method (offered alongside cards) lifts conversion 5–15% on consumer checkouts simply because buyers trust the wallet to handle disputes. Braintree gives you Stripe-like APIs with native PayPal, Venmo and pay-later support included.

Where it pinches

Native PayPal checkout is barely customizable; you cannot combine it with Apple Pay or Microsoft Pay in one flow. Pricing trends slightly higher than Stripe, dispute resolution is slower, and Braintree's CRM is thinner than Stripe's dashboard.

Reach for PayPal/Braintree when: the PayPal wallet button itself is a conversion lever for your buyers (consumer goods, donations, marketplace tipping) and you are willing to accept slightly higher fees in exchange.

Adyen and Worldpay: the enterprise interchange-plus tier

Once you cross roughly US$500K/mo in card volume, the conversation shifts from flat-rate to interchange-plus pricing. Adyen and Worldpay are the two names you will hear; both quote interchange + ~0.25–0.50% markup + a small fixed fee per transaction. Done right, this saves 60–120 bps versus Stripe at scale.

Why pick it

Native acquiring across multiple regions (so you settle in local currencies without forex losses), enterprise dashboards your CFO actually likes, deep local method coverage, dynamic 3DS routing that lifts authorization rates by 1–3 percentage points on EU traffic, and account managers who pick up the phone.

Where it pinches

Setup is heavier (KYC plus contract negotiation can take 4–8 weeks). Worldpay typically asks for a 3-year contract with US$295–$495 early-termination penalties. Both are awkward below US$200K/mo because the fixed fees and minimums eat any percentage savings.

Reach for Adyen / Worldpay when: monthly card volume is comfortably above US$500K, you process across 3+ regions, and the fee delta versus Stripe is bigger than the cost of a finance ops hire.

MangoPay and Razorpay: the regional specialists

Sometimes the right answer is not the global default. Two regional providers are worth a serious look when their geography matches yours.

MangoPay

EMI-licensed in the EEA and built around a wallet model: each user, seller and platform has a balance, and money moves between balances rather than through new card transactions. Excellent for marketplaces, crowdfunding, fan-economy products and anything that needs delayed payouts. Fees are typically lower than Stripe Connect at scale, but onboarding requires real KYC for both your platform and your sellers, and Apple/Google Pay are not native.

Razorpay

If your business is incorporated in India, Razorpay is the default. UPI, NetBanking and EMI options are first-class, fees are 2% domestic, and the dashboard is solid. Limitations are geographic: it does not work for non-Indian businesses, and Apple Pay is not supported. Many Fora Soft clients pair Razorpay (for India revenue) with Stripe (for the rest of the world) behind a single in-app pricing layer.

Reach for MangoPay / Razorpay when: 50%+ of revenue or the entire entity sits in one region (EEA or India) and you would rather optimize for local methods than for global breadth.

Need a second opinion on your provider mix?

Send your country, monthly volume and product type — we will benchmark Stripe, Adyen, MangoPay and Paddle against your actual numbers in a 30-minute review.

Merchant of Record (Paddle, Lemon Squeezy): pay 5% to delete tax pain

A Merchant of Record (MoR) is a third party that legally re-sells your product to the customer. Paddle, Lemon Squeezy (now part of Stripe) and FastSpring are the three names you will see. One honest caveat: the headline “all-in 5%” is rarely all-in once you sell cross-border — Paddle layers ~2–3% currency conversion and Lemon Squeezy adds ~1.5% on international cards, so a non-US seller’s effective rate can reach 7–8%. The MoR collects payment, charges the right VAT/sales tax for the buyer's jurisdiction, files those taxes, owns chargeback liability and remits a clean payout to you.

The trade you are making

You pay roughly 5% + $0.50 per transaction (vs. ~3% with a payment processor). In exchange you do not register for VAT in the EU, GST in Australia, sales tax in 45+ US states, JCT in Japan, KCT in Korea, etc. You also stop owning fraud and chargeback dispute work. For a B2C SaaS doing US$30K–$300K/mo across 20+ countries, the MoR fee is almost always cheaper than the all-in cost of a tax engine plus a part-time finance ops hire.

When the math flips

Above roughly US$500K/mo in B2C revenue, the 200 bps fee delta starts to outweigh the saved compliance work and you can profitably move to Stripe + Avalara/TaxJar/Stripe Tax. For B2B SaaS, where most invoices are tax-exempt anyway, MoR rarely makes sense from day one.

Reach for Paddle / Lemon Squeezy when: you sell digital goods or B2C SaaS to consumers in 10+ countries, your team is under 15 people and you want zero tax-registration work in year one.

The three monetization models that actually work — and how to wire each one

Across 20+ years of shipping software products, three monetization patterns cover almost every revenue model you will ship: one-time payments, subscriptions and marketplace splits. The remaining 10% (usage-based metering, in-app purchases, donations) are variants on these three. Each pattern implies a different webhook surface, a different idempotency model and a different failure mode.

Earning method 1: One-time payments (PPV, e-commerce, one-off buys)

A user pays once for a discrete unit: an e-commerce order, a movie rental on a video marketplace such as Vodeo, a single course purchase on an LMS, a credit pack in a B2B tool. Two implementation patterns dominate.

1. Hosted checkout (recommended). User clicks "Pay", you call your backend, your backend creates a Checkout Session with Stripe/Braintree/Adyen, browser is redirected to the provider-hosted page. Apple Pay, Google Pay, local methods, 3DS, receipts, refunds — all handled. Your work is one POST endpoint, one webhook handler and one success page. Engineering effort: 2–5 days for a clean integration.

2. Embedded Elements / Drop-in. Card form lives inside your UI; tokens are sent client-side to the PSP and never touch your servers. Higher conversion (no redirect), but you own more PCI scope (still SAQ A as long as the iframe is hosted by the PSP) and more failure-mode handling around 3DS challenges. Engineering effort: 1–2 weeks for a polished version.

Pick hosted unless conversion testing proves the redirect costs you more than 1.5% of orders. We recommend starting with Stripe Checkout and migrating to Elements only when product analytics demand it. For mobile apps that distribute through the App Store and Play Store, remember Apple and Google still require their billing for "consumable" or "non-consumable" digital content — see our deep dive on how to avoid Apple Pay commissions when the rules permit.

Earning method 2: Subscriptions (recurring billing done right)

Subscriptions are the highest-margin monetization model in SaaS, OTT, fitness, e-learning and telemedicine (if you’re building OTT/video specifically, our OTT platform guide goes deep on entitlement and churn). They are also the most punishing to get wrong, because every silent payment failure becomes recurring lost revenue.

Build vs. buy

For most products under US$5M ARR, Stripe Billing (~0.5–0.8% on top of card fees) does the job: trials, prorations, upgrades, downgrades, dunning, customer portal, MRR analytics. Above that, the limits show up: complex billing rules, deep ASC 606 revenue recognition, multi-product enterprises with custom contracts. That is where Chargebee or Recurly start to earn their seat. Chargebee plans run free for sub-US$250K ARR and scale to roughly US$599/mo at US$100K/mo billed; Recurly's edge is its ML-driven dunning, which often recovers an extra 3–5 percentage points of failed charges.

What you must wire from day one

Idempotent webhook handling for invoice.payment_succeeded, invoice.payment_failed and customer.subscription.updated; smart retries with exponential backoff; a customer portal so users can update cards without emailing support; an "involuntary churn" alert when a card declines so you can recover the user before they cancel mentally. Skipping any of these costs roughly 4–8% of MRR every year.

A working subscription stub

// Node + Stripe: idempotent webhook handler

import express from 'express';

import Stripe from 'stripe';

const stripe = new Stripe(process.env.STRIPE_SECRET);

const app = express();

app.post('/webhook', express.raw({type: 'application/json'}),

async (req, res) => {

const sig = req.headers['stripe-signature'];

let event;

try {

event = stripe.webhooks.constructEvent(

req.body, sig, process.env.STRIPE_WEBHOOK_SECRET);

} catch (err) {

return res.status(400).send(`Bad signature: ${err.message}`);

}

// Dedup by event.id BEFORE doing any work

if (await alreadyProcessed(event.id)) return res.json({received: true});

switch (event.type) {

case 'invoice.payment_succeeded':

await grantEntitlement(event.data.object);

break;

case 'invoice.payment_failed':

await scheduleDunning(event.data.object);

break;

case 'customer.subscription.deleted':

await revokeEntitlement(event.data.object);

break;

}

await markProcessed(event.id);

res.json({received: true});

});

Reach for Stripe Billing when: your pricing fits a small set of plans with simple add-ons; reach for Chargebee or Recurly when finance needs ASC 606 reports or your contracts include negotiated discounts.

Earning method 3: Marketplace splits (platform-to-user payouts)

A marketplace earns by taking a cut of payments that flow between buyers and sellers on the platform — ride-share rides, music licensing on Franchise Record Pool, fitness class bookings on AppyBee, course sales on Scholarly. Two architectural choices dominate.

Stripe Connect (recommended for early stage)

Three account flavours: Standard (seller manages their own Stripe dashboard), Express (Stripe-hosted onboarding under your branding) and Custom (you own every UI surface). Express is the right default — you skip the bulk of seller KYC, payouts go directly to seller bank accounts, and your platform fee is automatically deducted on each charge. Limitation: buyer and seller must usually be in countries Stripe supports for Connect (cross-border between the two is supported in the US and some EU corridors, not universally).

MangoPay or Adyen for Platforms (when you scale)

When your marketplace passes US$1M/mo or your sellers need wallet-style balances they can hold, withdraw and split themselves, MangoPay (EU-strong) and Adyen for Platforms (global enterprise) become attractive. Both are wallet-native, both support delayed payouts and split-on-withdrawal flows that Stripe Connect handles awkwardly.

Pitfalls unique to marketplaces

Refund liability (who eats the loss when a buyer disputes a long-completed purchase), tax obligations on the platform fee versus the underlying transaction, KYC for high-risk verticals, and seller payout timing. Get these into a written marketplace operating agreement before you ship.

Reach for Stripe Connect when: you are launching a marketplace, your buyer-and-seller mix is mostly within Stripe-supported countries, and you want shippable splits inside one sprint instead of one quarter.

Crypto and stablecoin payments: when 1% fees beat 2.9%

Crypto payments remain a niche — under 5% of consumer-facing businesses accept them — but they are growing in three specific lanes: cross-border B2B settlement, creator and gaming economies, and high-fee verticals where the 1% fee through Coinbase Commerce or BitPay (versus 2.9% on cards) materially moves margin. We have wired crypto into projects such as an NFT marketplace and covered the architecture in our deep dive on blockchain in mobile apps.

The two real options today

Coinbase Commerce. 1% flat fee. BTC, ETH, USDC, DOGE and others. Auto-settles to fiat or your wallet. The simplest way to add crypto to a checkout flow.

BitPay. Tiered: 2% + $0.25 below US$500K/mo, 1.5% under US$1M, 1% above. US$150 application fee with no approval guarantee. Daily fiat settlement is a real differentiator if your accounting cannot hold crypto on the balance sheet.

When stablecoins are the right answer

For cross-border B2B settlement specifically, USDC on Polygon or Solana settles in seconds at near-zero gas, with none of the volatility of BTC/ETH. Many fintech and Web3 platforms now offer USDC payouts as a primary rail; for traditional businesses it is still mostly a niche option, but worth designing the data model to support if your roadmap includes international payouts.

Reach for crypto rails when: your audience already holds wallets (gaming, NFT, Web3, expat remittance), card fees materially eat your margin, or you need cross-border B2B payouts in seconds rather than days.

PCI, PSD2/PSD3 and 3D Secure: what you must build vs outsource

Compliance is where most teams either over-engineer or quietly under-engineer. The simple rule: outsource everything you can, document the boundary clearly, and budget for the parts you cannot outsource.

PCI DSS scope

If card data never touches your servers (hosted Checkout or PSP-hosted iframe), you qualify for SAQ A — a short self-assessment, no audit. If you build a custom card form that posts to your servers, you fall into SAQ D, which means full PCI DSS 4.0.1 compliance — the version every 2026 assessment runs against, mandatory since 31 March 2025 (PCI SSC) — an annual QSA audit and US$5K–$50K of yearly compliance cost. We have not yet seen a SaaS or marketplace that benefits from SAQ D unless it is a payment company itself.

PSD2 SCA & the move to PSD3

Strong Customer Authentication is mandatory for payments where both buyer and seller are in the EEA. The implementation is 3D Secure 2 (3DS2): the issuing bank may pop a biometric or OTP challenge during checkout. Modern PSPs handle this automatically — but only if you actually use their recommended flow. A clumsy custom 3DS implementation can shave 5–10% of EU conversion. The right done-for-you implementation lifts authorization rates and stays out of the way.

Vertical-specific layers

Healthcare needs HIPAA-aware data handling around the buyer record and any clinical context (we cover this in our HIPAA-compliant video platform guide). Streaming and OTT often need geographic restrictions on entitlements. Marketplaces need clear seller KYC and tax-form generation (1099-K in US, DAC7 in EU). Decide what you must own and what your provider already covers before writing the first line of code.

Worried 3DS is hurting your EU conversion?

We will look at your authorization-rate dashboards and 3DS challenge logs in 30 minutes and tell you what is fixable this sprint.

Mini case: cutting payment ops on a video marketplace

Situation. Here’s a representative engagement — the figures are typical of this class of fix, not a single audited account. A subscription-plus-PPV video marketplace on Stripe Checkout had three problems: 6.4% involuntary churn from card declines, manual VAT calculations across 14 EU countries, and ~3.1% of subscribers re-creating accounts because the customer portal was missing. Combined leak: roughly US$11K of MRR every month at their scale.

The 12-week plan. Weeks 1–3: replace bespoke billing logic with Stripe Billing + Customer Portal. Weeks 4–6: enable Stripe Tax for the EU plus the US states with nexus. Weeks 7–9: build a smart-retry layer driven by invoice.payment_failed webhooks with exponential backoff, plus pre-dunning email sequence at day 3 and day 5. Weeks 10–12: instrument authorization-rate, decline-reason and recovered-charge dashboards.

Outcome. Authorization rate moved from 92.1% to 96.3%; involuntary churn dropped from 6.4% to 3.7%; manual finance ops time fell ~38% per month. Net: roughly US$8.4K/mo in recovered revenue at their scale, plus a finance team that stopped working weekends. Want a similar assessment for your stack? Book a 30-min payment-ops review.

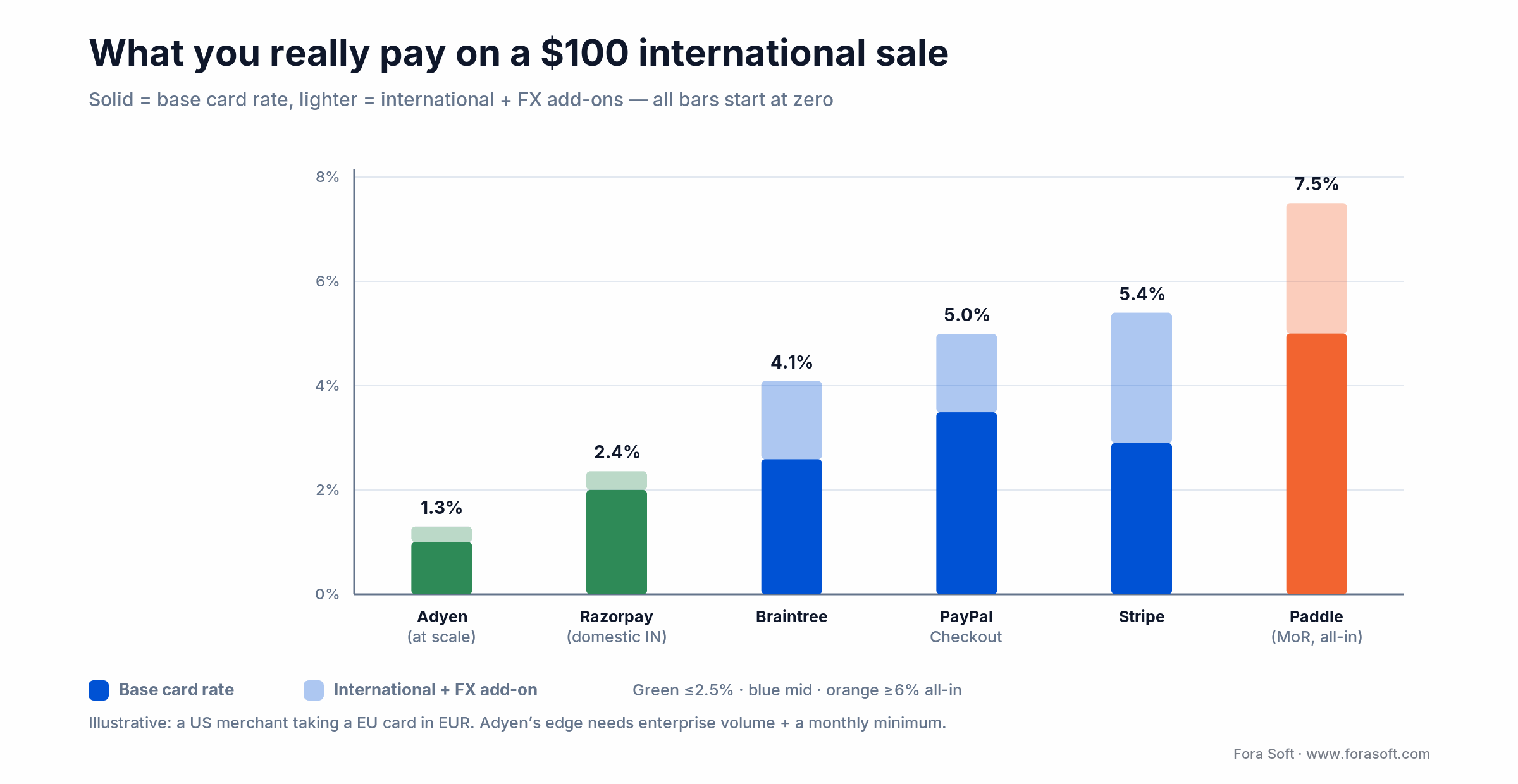

What a real payment integration costs in 2026

These are honest, conservative ranges for payment gateway integration run by a team using modern AI-assisted engineering. We deliberately under-promise — bespoke complexity (multi-region routing, heavy compliance, on-prem infrastructure) sits above these numbers and we will tell you that on the call.

Figure 4. Headline rates hide international and FX add-ons; the all-in number is what hits your margin.

| Scope | Typical effort | Realistic budget | Where it gets bigger |

|---|---|---|---|

| Stripe Checkout for one-time payments | 3–5 days | ~US$2K–$5K | Custom receipts, refund flows |

| Subscription billing on Stripe Billing | 1–2 weeks | ~US$5K–$12K | Trials, upgrades, dunning UX |

| Stripe Connect marketplace | 3–5 weeks | ~US$15K–$35K | Seller KYC, payout schedules, escrow |

| Multi-provider routing (Stripe + Razorpay + Coinbase) | 6–10 weeks | ~US$30K–$70K | Reconciliation, ledger, fraud rules |

| Migration from PSP A to PSP B | 4–8 weeks | ~US$20K–$50K | Tokenization migration, dual-write window |

For a more detailed budgeting model on the surrounding software (video player, platform, mobile shells, infrastructure), see our video platform development cost guide and the streaming platform cost breakdown.

Five payment pitfalls that quietly burn revenue

1. Webhook drift. Stripe and most PSPs do not guarantee delivery order; the same event can arrive twice. If you increment an account balance directly on every charge.succeeded without checking the event ID, you double-credit users. Always dedupe by event ID and use idempotency keys on every state-changing call. The dedicated payment system testing process we run on every Fora Soft engagement is built around exactly this kind of failure mode.

2. Idempotency keys missing on retries. When a network blip causes a retry, a missing idempotency key means the second call processes a fresh charge. We have seen real teams ship US$40K of duplicate charges in a weekend. Stripe and Adyen both cache the response by idempotency key for 24 hours, costing you nothing extra to use them.

3. FX losses through bank wires. A B2B SaaS billed in USD but paying out in EUR via wire transfer can leak 1–3% per cycle to bank FX spreads. Multi-currency Stripe accounts, Wise Business or Adyen native settlement collapse this to 25–50 bps.

4. Fragile 3D Secure flows. Custom 3DS modals that do not handle network errors, popup blockers or returning users gracefully can cost 5–10% of EU checkout conversion. Use the PSP's native SCA flow; if you need to brand it, brand the wrapper, not the challenge itself.

5. Unregistered VAT obligations. The first time a US-incorporated SaaS hits the registration threshold in Germany or France without noticing, the back-tax bill plus penalties can wipe a quarter of MRR. Either use a Merchant of Record from day one (Paddle, Lemon Squeezy) or wire Stripe Tax / Avalara from launch.

KPIs to monitor from day one

Quality KPIs. Authorization rate (target >95%, alarm below 92%), decline rate by reason code (catch issuer-specific spikes), 3DS challenge rate and 3DS abandonment rate (target <15% abandonment), chargeback rate (Visa monitoring threshold is 0.9% — alarm at 0.5%).

Business KPIs. MRR and ARR with daily granularity, gross vs. net revenue retention (NRR >100% means expansion is outrunning churn), LTV/CAC (target 3:1 minimum for SaaS), refund rate by SKU.

Reliability KPIs. Webhook success rate (alarm if any handler <99.5% over 24h), failed-charge recovery rate (Chargebee/Recurly dunning typically recovers 8–15% — under 5% means your retry strategy needs work), payout reconciliation lag (alarm if >48h).

When you should not build custom payments at all

A few honest cases where the smart move is to skip building anything and ship faster.

- Pure consumer digital downloads in 20+ countries. Use Lemon Squeezy or Paddle, ship in a weekend, never think about VAT.

- Mobile-first apps with consumable IAP. Apple StoreKit and Google Play Billing are mandatory for in-app digital content; trying to route around them gets your app de-listed.

- Donations and tipping. Stripe's hosted Payment Link or PayPal Donate Lite get you 90% of what you need with zero engineering.

- Internal-tools billing inside a small team. A Stripe customer portal link in a Slack message is faster than building a billing UI.

- Gambling, adult, certain crypto verticals. Build with a vertical-specialist provider (Worldpay High Risk, Nuvei) from day one; do not waste time on Stripe applications that will be denied.

Reach for "do not build" when: the time you would spend on payments would meaningfully delay the actual product, and an off-the-shelf solution covers 95% of the use case.

FAQ

Which payment provider should a US-incorporated SaaS use in 2026?

Stripe is the safe default below US$1M/mo, with Stripe Tax bolted on for sales-tax compliance. Above that, run a real interchange-plus quote against Adyen and decide based on the absolute fee delta and your finance team's appetite for a longer integration.

When does a Merchant of Record like Paddle make more sense than Stripe?

B2C digital products selling globally to consumers, where VAT/GST in 20+ countries would otherwise consume real engineering and finance ops time. Below ~US$500K/mo in B2C revenue, the 200 bps fee delta is almost always cheaper than the alternative.

How long does a Stripe integration actually take?

A clean hosted Checkout for one-time payments lands in 3–5 days. Subscription billing with proper webhooks, dunning and a customer portal lands in 1–2 weeks. A Stripe Connect marketplace with seller KYC, splits and payouts is 3–5 weeks of focused work.

What is the difference between hosted checkout and embedded payment forms?

Hosted checkout redirects buyers to a PSP-hosted page (highest security, lowest engineering effort, slight conversion cost from the redirect). Embedded forms (Stripe Elements, Braintree Drop-in) live inside your UI as PSP-hosted iframes — better conversion, more polish, slightly more PCI-scope work. Start hosted, migrate to embedded only if conversion data demands it.

Do you need a separate provider for crypto payments?

If you only occasionally see crypto buyers, no — the integration cost is not worth it. If you are in a vertical where 5% or more of buyers prefer crypto (gaming, NFTs, expat remittance, certain B2B cross-border) plug in Coinbase Commerce or BitPay alongside your card processor and let users self-select.

How do you keep PCI scope as small as possible?

Never let raw card data hit your servers. Use hosted Checkout or a PSP-hosted iframe for the card form, store only the PSP's tokens, and verify your network/cloud configuration restricts the card-form domain to the PSP. That keeps you on SAQ A — a self-questionnaire instead of a US$10K–$50K annual audit.

What does PSD3 change in 2026 and 2027?

PSD3 extends Strong Customer Authentication beyond cards to instant payments, BNPL and crypto, tightens fraud-rate thresholds for SCA exemptions, and unifies licensing across the EEA. The day-to-day for most builders stays the same: keep using your PSP's native 3DS flow and the changes will land at the provider layer.

Can you use Stripe and Razorpay together?

Yes — we ship this regularly. Route Indian buyers (or any buyer with an Indian card BIN) to Razorpay and everything else to Stripe behind a single in-app pricing layer. Razorpay's ~2% domestic vs. Stripe's ~3.5% on international Indian cards usually pays for the routing layer in the first month.

What to read next

Quality & QA

How to test a payment system properly

The exact reliability process we run on every Stripe and Adyen rollout we ship.

Monetization

Video streaming app monetization strategies

SVOD, AVOD, TVOD, hybrid — the trade-offs and which one fits which product.

Mobile

How to (legally) avoid Apple's 30% commission

Where Apple's billing rules permit web checkout, and where they do not.

Go-to-market

Getting your first paid user

A pragmatic playbook for turning a working payment integration into actual revenue.

Blockchain

Blockchain in mobile apps

When crypto and stablecoin payments make sense as a real channel, not a marketing line.

Ready to ship a digital payment solution that converts?

A digital payment solution is rarely the most exciting part of your product, but it is the part that quietly decides whether the business survives. Pick the provider before the feature set, design for the monetization model from day one, push every PCI obligation you legally can to the PSP, and instrument enough KPIs to spot revenue leaks the day they start.

If you want a second pair of eyes on the choice between Stripe, Adyen and Paddle — or you already have the integration and want to recover the last 200–400 bps that bad webhooks and weak 3DS are costing you — we have spent two decades doing exactly that work. That’s 250+ products since 2005, built by a 50-engineer in-house team, and payments usually ship as part of a wider custom software development or dedicated team engagement.

Want a payments architecture that pays for itself?

30 minutes with our team will give you a concrete provider recommendation and a punch list of revenue-recovery wins for your current stack.